Our firm is committed to complying with the "AssurMiFID Rules of Conduct" and, in this regard, communicates to you the following information:

1. Products and services offered

1.1 Information on concept of insurance mediation

"Our firm offers services of insurance mediation, i.e. the activities that consist in advising on insurance contracts, offering, proposing, carrying out preparatory work for the conclusion of insurance contracts or concluding insurance contracts, or assisting in their administration and execution."

1.2. Branch numbers and titles

1: Accidents;

2: Illness;

3: Vehicle airframe excluding railway rolling stock;

5: Aircraft airframe;

6: Marine and inland waterway hulls;

7: Goods transported including merchandise, baggage and all other goods;

8: Fire and nature events;

9: Other damage to goods;

10: BA motor vehicles;

11: BA aircraft;

12: BA sea and inland vessels;

13: General BA;

14: Credit;

15: Bail;

16: Various cash losses;

17: Legal aid;

18: Assistance;

21: Life insurance - not linked to investment funds, except dowry and birth insurance;

22: Dowry and birth insurance, not linked to mutual funds;

23: Life, dowry and birth insurance related to mutual funds;

26: Capitalisation operations;

27: Management of collective pension funds.

1.3 Policy conditions

View our document centre

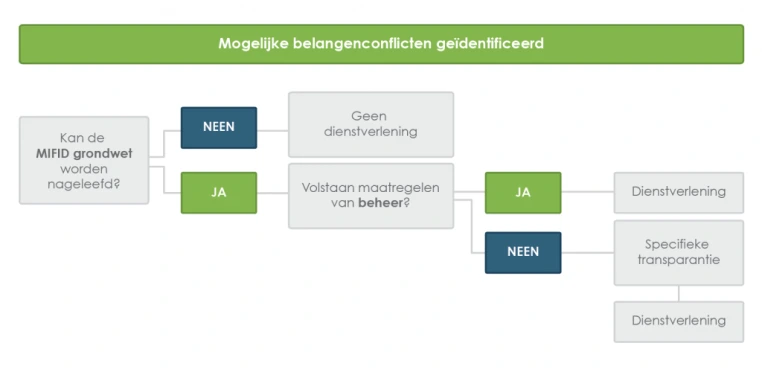

2. Information on the conflict of interest policy

The AssurMiFID rules of conduct require our firm to establish a written policy for managing conflicts of interest. More information on how our firm complies with this can be found below.

2.1. Legislative framework

From 30 April 2014, the "AssurMiFID rules of conduct" are in force. They find their legal basis in the Act of 30 July 2013 to strengthen the protection of the buyers of financial products and services as well as the powers of the FSMA and various provisions as well as the Royal Decree of 21 February 2014 on the rules of application of articles 27 to 28bis of the Act of 2 August 2002 on the supervision of the financial sector and financial services to the insurance sector and Royal Decree of 21 February 2014 on the rules of conduct and rules on the management of conflicts of interest adopted pursuant to the Act, as far as the insurance sector is concerned. In accordance with these rules of conduct, our firm is required to draw up a written policy on the management of conflicts of interest when providing insurance mediation services. The legal regulation on conflicts of interest complements the general MiFID constitution. This constitution is respected by our firm by acting loyally, fairly and professionally in the client's interests when providing insurance mediation services.

2.2. What conflicts of interest?

For the purpose of our conflict of interest policy, our firm has, in a first step, identified the potential conflicts of interest in our firm. Conflicts of interest may arise between (1) our firm and its related persons and a client or (2) between several clients. The conflict of interest policy takes into account our firm's own characteristics and its group structure, if any. In assessing for potential conflicts of interest, our firm has identified those situations where there is a significant risk of harming clients' interests. These include:

- Situations where profits are made or losses incurred at the expense of the client;

- Situations where our firm has another interest in the outcome of the service or transaction;

- Situations with a financial incentive to put other clients ahead;

- Situations involving the same business as the client;

- Situations where our firm receives compensation from a person other than the client for insurance mediation services rendered;

- Situations where our firm holds stakes of at least 10% in voting rights or of the capital of the insurance company(ies);

- Situations where the insurance company(ies) holds stakes of at least 10% of the voting rights or capital of our firm.

2.3. What measures does our office take?

Our firm takes many measures to ensure that the client's interests prevail. These include:

- An internal instruction note;

- An adapted remuneration policy;

- A policy to ensure that related persons only mediate on insurance contracts whose essential characteristics they know and are able to explain to clients;

- A policy that reserves the right of our firm to refuse the requested service in the absence of a concrete solution to a specific conflict of interest with the sole purpose of protecting the client's interests;

- An arrangement on receiving benefits;

- A policy to ensure that all information provided by our related persons is accurate, clear and not misleading.

- If necessary, our firm's conflict of interest policy will be amended and/or updated.

2.4. What is the procedure?

2.5. Specific transparency

If, in a concrete situation, our measures might not provide sufficient guarantee, you will be informed by our office about the general nature and/or sources of the conflict of interest so that you can make an informed decision. You can always contact us for more information.

3. Reimbursement

For our services of insurance mediation, we basically receive a fee from the insurance company, which is part of the premium you pay as a client. In addition, a fee associated with our office's insurance portfolio with the respective insurance company or for additional tasks completed by our office is possible. For more information contact us. Otherwise, for our services of insurance mediation, we receive a fee from you as a client.

4. Complaints clause

Our office is registered in the register of insurance intermediaries maintained by the FSMA, at 1000 Brussels, Rue du Congrès 12-14 and can be found at http://www.fsma.be. For all your questions and problems, please contact our office in the first instance. We can always be reached by phone, e-mail or fax. Complaints can also be submitted to the Insurance Ombudsman's Office at 1000 Brussels, de Meeûssquare 35, tel. 02/547.58.71 - fax. 02/547.59.75 - info@ombudsman-insurance.be - www.ombudsman-insurance.be * Law of 30 July 2013 to strengthen the protection of the buyers of financial products and services as well as the powers of the FSMA and various provisions as well as the Royal Decree of 21 February 2014 on the rules of application of articles 27 to 28bis of the Law of 2 August 2002 on the supervision of the financial sector and financial services to the insurance sector and Royal Decree of 21 February 2014 on the rules of conduct and rules on the management of conflicts of interest adopted pursuant to the Law, as regards the insurance sector.